Life Insurance Myths: Debunked

Though we don’t like to think about it, all of us will make an exit sometime. Are you prepared?

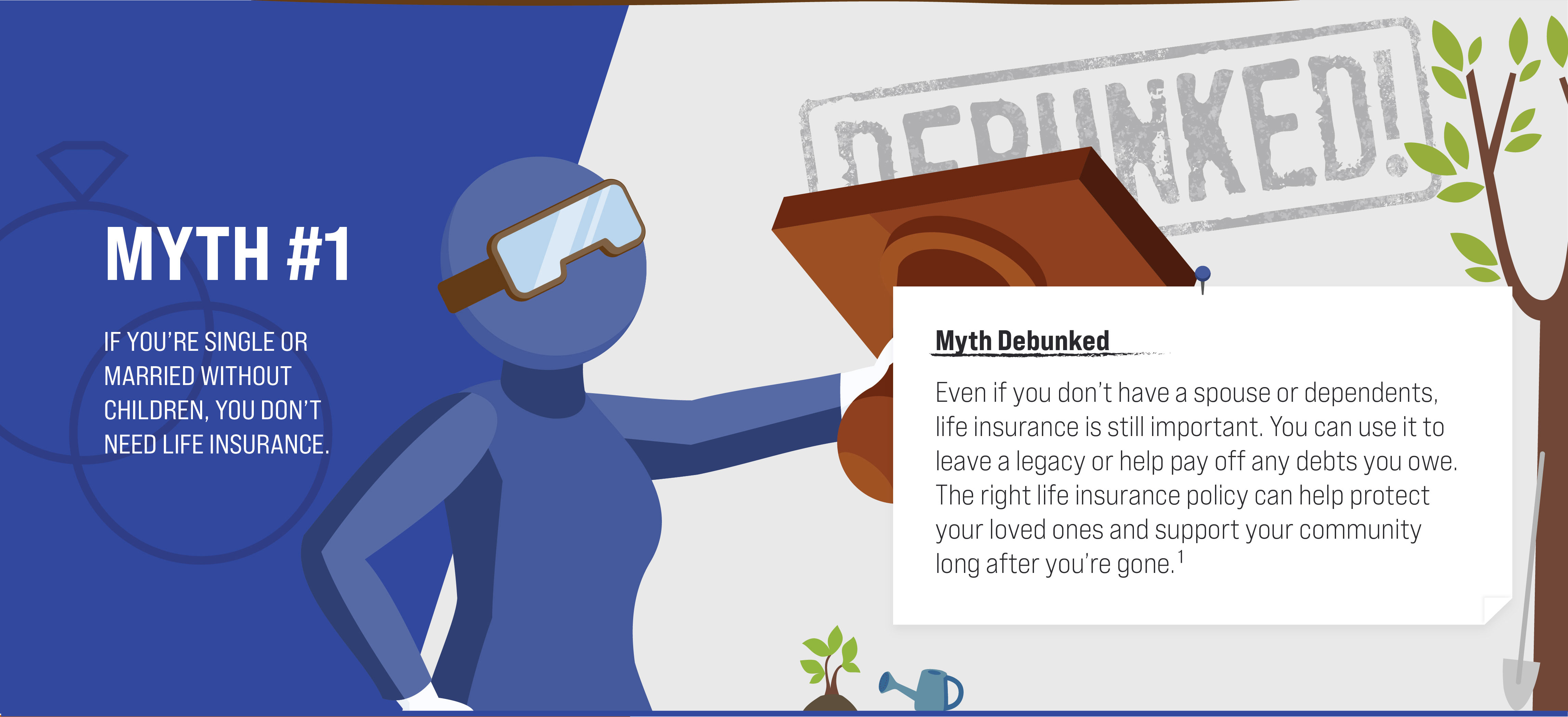

Even if you’re young and single, you should still consider protecting yourself.

The chances of needing long-term care, its cost, and strategies for covering that cost.