Disability and Your Finances

The Social Security Disability Insurance program is projected to pay out approximately $133 billion in benefits in 2020. And with new applicants each year, the system is expected to exhaust its reserves at the end of 2035 if changes aren’t made.1,2

Rather than depending on a government program to protect their income in the event of a disability, many individuals prefer to protect themselves with personal disability insurance.3

Disability insurance provides protection by replacing a portion of your income, usually between 50 percent and 70 percent, if you become disabled as a result of an injury or illness. This type of insurance may have considerable benefits since a disability can be a two-fold financial problem. Those who become disabled often find they are unable to work and are also saddled with unexpected medical expenses.

What About Workers Comp?

Many people think of workers compensation as a disability safety net. But workers compensation pays benefits only to individuals who become disabled while at work. If your disability is the result of a car accident or other off-the-job activity, you may not qualify for workers compensation.

Even with workers compensation, each state makes its own rules about payment and benefits, so coverage may vary considerably. You might consider finding out what your state offers and plan to supplement coverage on your own, if necessary, especially if you have a high-risk profession. Likewise, if you have an active lifestyle that puts you at a higher risk of disability, considering an extra layer of protection may be a sound financial decision.

If you become disabled, personal disability insurance can be structured to pay a benefit weekly or monthly. And benefits are not taxable, if you have paid the premiums in full.4

When you purchase a policy, you may be able to tailor coverage to suit your needs. For example, you might be able to adjust benefits or elimination periods. You might opt for comprehensive protection or decide to define coverage more specifically. Some policies also offer partial disability coverage, cost-of-living adjustments, residual benefits, survivor benefits, and pension supplements. Since coverage is designed to replace income, most people choose to purchase protection only during their working years.

Even as changes are made to federal disability programs, they typically provide only modest supplemental income, and qualifying can be difficult. If you don't want to rely solely on Uncle Sam in the event of an unforeseen accident or illness, disability insurance may be a sound good way to protect your income and savings.

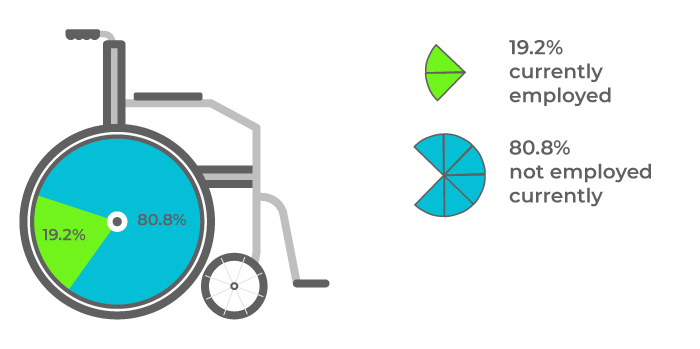

Out of Commission

According to the most recent data available, about 19.2 percent of working-age disabled Americans are employed.

Source: ACLI Life Insurers Fact Book, 2019

1. Social Security Administration, 2020

2. Barron’s.com, 2019

3. Disability insurance is issued by participating insurance companies. Not all policy types and product features are available in all states. Any obligations are dependent on the ability of the issuing insurance company to continue making claim payments.

4. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Federal and state laws and regulations are subject to change, which would have an impact on after-tax investment returns. Please consult a professional with legal or tax experience for specific information regarding your individual situation.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.