A Primer on Irrevocable Life Insurance Trusts

"I’m proud to pay taxes in the United States; the only thing is, I could be just as proud for half the money."

Entertainer Arthur Godfrey

The irrevocable life insurance trust (ILIT) can be an important estate strategy tool that may accomplish a number of estate objectives; however, it may not be appropriate for every individual.1,2

What Is an ILIT?

An ILIT is created by an individual (the grantor) during his or her lifetime. The ILIT owns a life insurance policy on the grantor’s life via the transfer of ownership of an existing policy or through the grantor’s annual contribution of cash to pay the premiums on a policy purchased by the trust.3

The grantor designates beneficiaries, usually family members, who will typically receive the proceeds upon the death of the grantor.

The trust is irrevocable, meaning that the grantor forfeits all rights to the property contained in the trust. Its irrevocable nature is integral to accomplishing the ILIT’s objectives.

What Can an ILIT Accomplish?

The ILIT may be able to accomplish several estate objectives, including:

- Meeting liquidity needs;

- Managing estate taxation on the policy proceeds;

- Providing income to survivors.

How Does an ILIT Work?

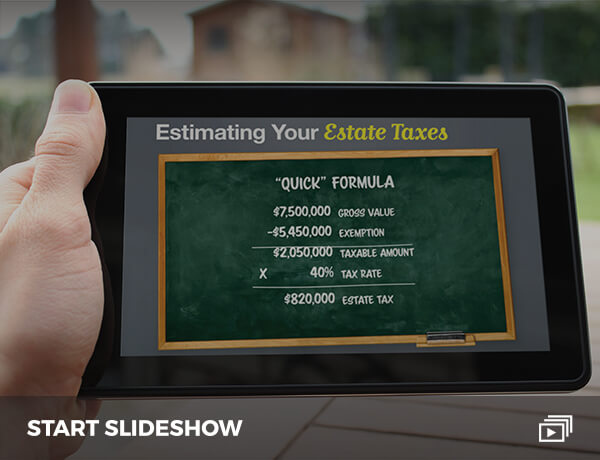

When you die, the trust is designed to receive a payment equal to the policy coverage amount, e.g., $500,000. Since the trust’s ownership of the policy is irrevocable, the proceeds are not considered your property. Consequently, they do not fall into your estate, thus potentially avoiding estate taxation. (Remember, generally no income tax is due on such life insurance proceeds.)4

The trust provisions should be set up to provide direction about how and to whom payments may be made. You may direct that the trust pay out cash to cover certain expenses, e.g., funeral costs, probate, taxes, final medical expenses, and debts.

This may obviate the need to sell less liquid assets at an inopportune time to cover such costs.

The trust’s beneficiaries may receive the proceeds (after any payments are made to satisfy liquidity needs), creating an inheritance free of estate taxes. Finally, creditors should not be able to attack these assets since they belong to the trust, not you.

Creating an ILIT should be done only with the assistance of a qualified estate planning attorney. It is a complicated exercise in which mistakes may result in losing the benefits ILITs offer.

1. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

2. Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

3. Investopedia.com, 2021

4. This is a hypothetical example used for illustrative purposes only. It is not representative of any specific estate or estate strategy. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright FMG Suite.